The U.S. Geological Survey (USGS) categorizes volcanic hazard zones to assess the risk of lava flows. For Maui:

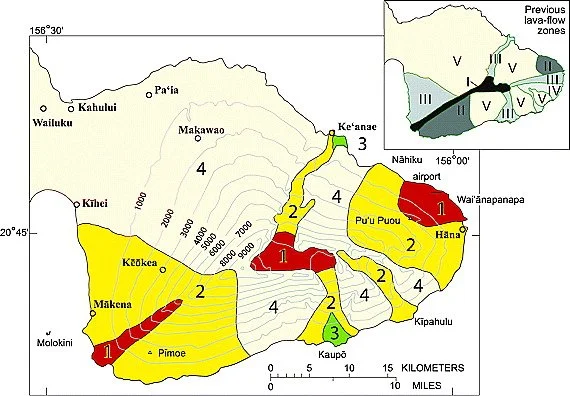

Zone 1 and Zone 2: These are areas with the highest risk of lava flows, but in Maui’s case, since the volcanoes are dormant or extinct, these zones don’t currently reflect an immediate threat. However, historically, these zones would be where lava flows were most likely if an eruption were to occur.

Lower Zones (3-9): These zones represent decreasing levels of hazard, with Zone 9 being the least hazardous. On Maui, these zones would still be mapped based on historical data and topography, but the risk is significantly lower due to the dormancy of Haleakalā and the extinction of the West Maui volcano.

Volcano Insurance in Maui County:

Given the dormant status of Haleakalā and the extinct nature of the West Maui Mountains, here’s how insurance works:

Standard Homeowners Insurance: Most standard homeowners insurance policies in Maui might not specifically mention “volcano insurance” since the risk of an eruption is very low. However, they generally cover damage from fires caused by lava flows or ash if such an event were to occur, as these would be considered under fire damage.

Lava Flow Coverage: Since there’s no specific “volcano insurance,” coverage for lava flow damage would be rare unless explicitly added as an endorsement or if it’s included in a comprehensive policy. For dormant volcanoes like Haleakalā, this is less of a concern, but if you live in a historical high-risk zone (like Zone 1 or 2), some insurers might offer additional coverage or endorsements for volcanic activity at a higher premium.

Hawaii Property Insurance Association (HPIA): For those in high-risk zones where private insurers might not offer coverage or offer it at very high rates, the HPIA provides insurance as a last resort. However, because the risk in Maui is minimal due to the dormancy, most homeowners might not need to turn to HPIA unless for other reasons like cost or specific policy exclusions.

Insurance Considerations: Since the volcanoes are not currently active, insurance premiums in Maui are more influenced by other factors like wildfires and hurricane risk, which is a significant concern given Hawaii’s location. Still, if you’re in a historically high-risk lava zone, you might want to:

Check if your policy includes any volcanic activity coverage.

Ask your insurer about additional endorsements if you want extra peace of mind.

Consider the cost-benefit since the actual risk of an eruption is low.

In summary, in Maui County, while the concept of volcano zones exists, the practical risk is minimal due to the dormancy of Haleakalā and the extinction of the West Maui Mountains. Volcano insurance isn’t typically a focal point, but understanding your policy’s coverage for potential fire damage, flood damage, and wind damage would be a good idea. For more detailed information, consult with an insurance agent specializing in Hawaiian properties or check in with Jamie Peacock of Insurance Associates.

Volcano Zones in Maui County:

Haleakula is considered “dormant” and hasn’t erupted for about 400 years*

Maui County has two main volcanic structures: Haleakalā and the West Maui Mountains (Mauna Kahalawai). Here’s how these relate to volcano hazard zones:

Haleakalā: This is the larger of the two and is considered dormant. Its last eruptions occurred between 1480 and 1600, according to geological records. Despite being dormant, it’s still classified as an active volcano by the USGS due to potential future activity, but currently, it’s in a non-eruptive state.

West Maui Mountains: This volcano last erupted over 320,000 years ago, making it effectively extinct.